Lock-In Effect: What to Expect in the 2024 Florida Housing Market

Tue Jan 30, 2024 on Florida Real Estate

Now that we are into the New Year and the dust is beginning to settle, it is becoming apparent that residential real estate prices reached their peak late last year. In fact, now we are experiencing housing prices decline in many residential real estate markets in South Florida. The real culprit for prices not lowering quicker is the fact that there is an incredible lack of supply. Economists called this real estate situation the “lock-in effect” which essentially means that homeowners are not willing to sell their homes because they effectively have nowhere to go and that they are locked in. Why? Homeowners may think that they are locked in first and foremost because if they have a mortgage, that mortgage will likely be well below 6 percent, and mortgage rates currently still hover well above 6 percent. In fact, many homeowners have mortgages at 3, 4, and 5 percent, so should a homeowner wish to move to a new home and require a mortgage, that homeowner may not be able to afford that new home because the new mortgage payments would most likely exceed what they are currently paying.

In addition to the “lock-in effect”, Florida has a real estate homestead tax portability which allows a homeowner to transfer or “port” to a new homestead in Florida all or part of one’s homestead assessment difference. However, the fact is that most people’s homes, if they have been in them for a long time, are assessed well below value, and anyone who buys a new home will most likely be paying more taxes and again have an increase in their monthly expenses.

As a result of both the lock-in effect and residential real estate assessments, the number of sales of homes in South Florida, and for that matter the entire country, was at a 28-year low for 2023.

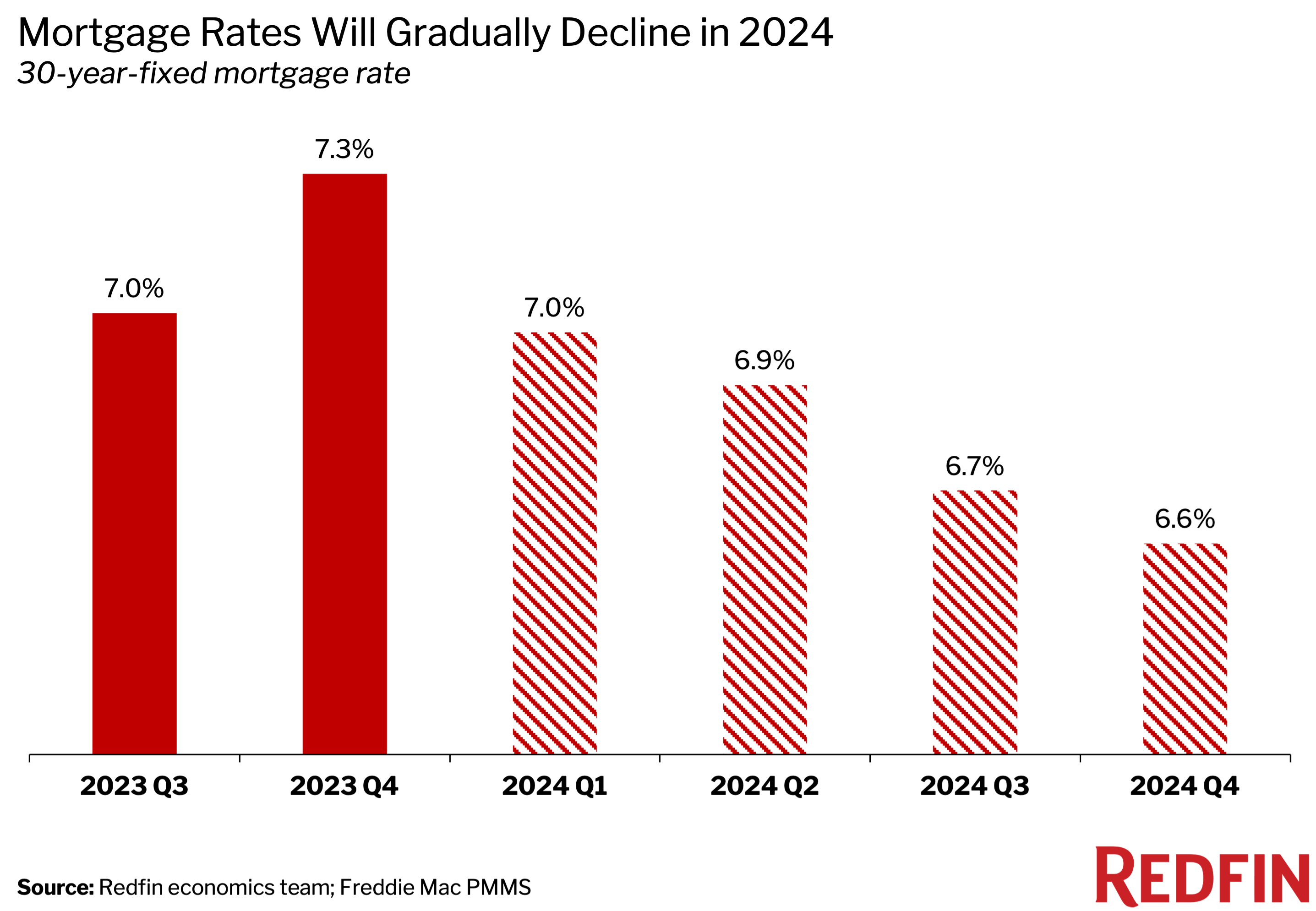

The good news is that since we are in an election year, it is fully anticipated that interest rates will start to lower and with that there will be a thaw in the few listings that currently exist. Most economists, including the folks at Fanny Mae, are anticipating that interest rates will drop, bringing more sellers who were on the sidelines contemplating selling actually listing their homes. In fact, there is supposedly huge pent up demand for sellers who need or want to sell their homes.

If there are new listings will that necessarily mean that prices will stay the same, go up or go down? The answer to that is, of course, it all depends. If in fact there are lots of residential home buyers who have been waiting for interest rates to drop in order to afford a home, then, in theory, there could be an equilibrium between buyers and sellers. If there are more listings than buyers, and thus more supply, prices would drop as they are currently doing.

In fact, that is exactly what economists at the Federal Reserve are attempting to achieve as they believe that home prices need to decrease in order to make homes more affordable again. Many people currently cannot afford a new home because they do not have enough income to support a high interest rate mortgage, certainly not at 6 or 7 percent.

If mortgage rates only come down to about 5 percent, which is the historical average, then current prices would still be too high and continue to not allow a large segment of the population to enter the home ownership market. Thus, it is likely that interest rates will come down slightly, just enough to get folks out of their current homes and list those homes, but not necessarily create a new demand for new buyers. If in fact that were to happen, then prices will continue to drift downward. They likely will not drift downward to the point that the Federal Reserve wants but will still nevertheless allow more buyers ultimately to come back into the market and thereby allow prices to then start slowly rising again.

So, what does this all mean?

It means if you are a residential real estate buyer, you may wish to start looking at the market to see what values are currently, so when you see a deal you’ll know it will be a good time to proceed or in the alternative, there may be good deals that are already popping up because certain sellers are in a position where they will not wait any longer because they are not affected by interest rates. Such sellers include those who do not have a mortgage, estates or where people are moving out of the area to be closer to other family members or other domestic situations that require the house to be sold immediately.

And if you are a seller, you probably would be better off selling now than before there is a deluge of new listings that come on the market.

Similarly, in the preowned condo environment, as special assessments start to percolate through the system in order to make repairs and to ensure infrastructure of such buildings, it may be best to sell now before you are competing with too many sales within your own building.

Finally, one interesting tidbit that has not been discussed much in the news is that there is a fair amount of refinancing going on currently. People are not refinancing their first mortgages in order to get a better rate, but rather they are refinancing their mortgages in order to get more equity out of their homes, so that they can pay down very expensive credit card debt.

Over the 30-plus years that I have been in the real estate market, when homeowners start to refinance either to pull equity out and invest in the stock market which occurred in the early 2000s or when they started pulling cash out to pay down expensive credit card debt, this is usually a sign that this is the end of a sellers’ market and that prices have peaked. The problem, of course, is that the excess equity in people’s homes historically has served as a cushion or safety net in the event someone loses their job, a wage earner gets sick or if there is a divorce. When that equity is used to pay down debt, that safety net is removed, and if the economy were to take an unexpected dive because of a potential unexpected exogenous event, people in those situations will possibly put themselves in a vulnerable position and conceivably could have their house foreclosed out from under them.

In any event, if you are in the real estate industry, it appears that the worst may well be over and that things will be picking up in 2024.

From the Trenches,

Roy Oppenheim

originally posted at: https://www.oppenheimlaw.com/news-resources/lock-in-effect-what-to-expect-in-the-2024-florida-housing-market/